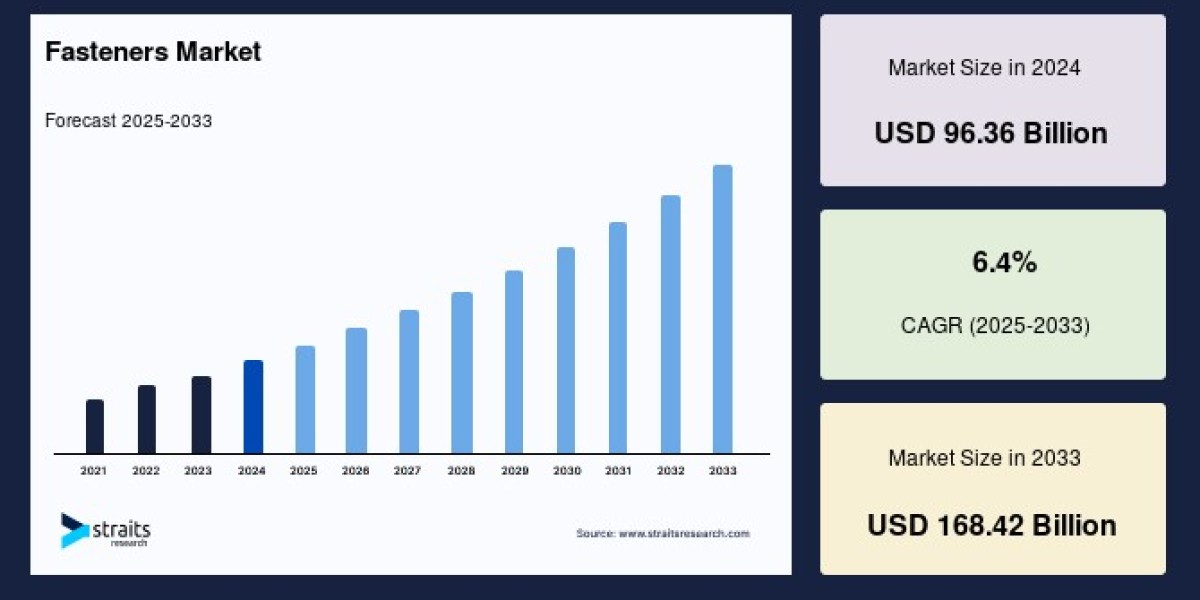

The global fasteners market is witnessing significant expansion, valued at USD 96.36 billion in 2024 and poised to grow to USD 168.42 billion by 2033, reflecting a healthy compound annual growth rate (CAGR) of 6.4% during 2025-2033. This vigorous growth is fueled primarily by rapid industrialization, infrastructure development, and rising demand from the automotive, aerospace, construction, and industrial machinery sectors.

Market Overview and Growth Dynamics

Fasteners components such as bolts, screws, nuts, rivets, studs, and anchors are essential for joining two or more parts to form a unified functional product. They are critical across diverse industries where mechanical strength, durability, and reliability are paramount. The evolving end-use industries are increasingly demanding fasteners that not only provide superior performance but also meet enhanced aesthetic and quality standards, driving innovation towards specialty fasteners with unique materials and designs.

The substitution trend where plastic fasteners are replacing traditional metal fasteners is emerging as a key growth avenue. Plastic fasteners offer attractive benefits such as lower weight and cost, making them an ideal solution in industries focused on lightweight components, most notably in automotive manufacturing.

Specialty Fasteners: Rising Demand and Innovations

Specialty fasteners differ from standard fasteners mainly in design, materials, and head styles. They often incorporate materials like titanium, brass, and bronze, designed to perform under extreme conditions including corrosion, vibration, and severe impacts. As manufacturers in various end-use industries emphasize final product durability and appearance alongside functionality, specialty fasteners have gained considerable traction.

Customization through modification of existing designs to produce non-standard fasteners enables manufacturers to cater to niche and demanding applications. Such innovation is projected to fuel specialty fasteners market growth beyond that of conventional fasteners.

Regional Market Landscape

Among the global regions, Asia-Pacific holds the largest market share and is the fastest growing region with a CAGR of 7.3%. The region, led by countries such as China, India, and Japan, benefits from robust automotive production, expanding industrial machinery manufacturing, increasing electronics demand, and rapid infrastructure development. China’s status as the largest automotive market globally, with over 28 million vehicles sold in 2020 alone, strongly propels demand for automotive fasteners.

Europe holds the position of the second largest market and is characterized by high demand driven by advanced automotive manufacturing hubs in Germany, the UK, Italy, and France. The European market is forecast to grow at a CAGR of approximately 6.2%, supported by ongoing innovations toward lightweight and high-strength vehicles. North America ranks third, with the U.S. leading fastener demand due to a broad automotive, aerospace, and industrial manufacturing base. The U.S. aerospace manufacturing sector, with key players like Boeing and Lockheed Martin, significantly contributes to market growth.

Application Segments: Automotive and Construction Lead

The automotive industry represents the largest application segment for industrial fasteners. Fasteners are integral to assembling various critical automotive components such as engines, suspension systems, and braking assemblies. The automotive fasteners market witnesses sustained demand driven by high vehicle production volumes in emerging economies and technological shifts towards electric vehicles.

The construction sector is another major driver for fastener demand. Metal fasteners dominate this segment due to their superior strength and corrosion resistance compared to plastics. They are extensively used for bonding, attaching panels, cable management, and structural connectivity in buildings, bridges, and infrastructure projects. Increasing infrastructure investments and rising demand for single-family homes in regions like North America are expected to further fuel market growth.

Material Insights: Steel Dominates

Steel constitutes the primary raw material for industrial fasteners, thanks to its excellent mechanical properties, tensile strength, and resistance to corrosion when stainless or coated. The fastener industry utilizes various steel grades, including martensitic, ferritic, and austenitic stainless steels, depending on application requirements for temperature tolerance and strength.

Other materials gaining ground include aluminum and specialty alloys such as titanium for aerospace applications, prized for their combination of high strength and low weight. However, the growing preference for lightweight automotive components is pushing the adoption of alternative materials like plastics and hybrid fasteners composed of plastic-metal composites.

Challenges and Emerging Substitutes

Despite its robust outlook, the metal fasteners market faces challenges from rising metal prices and growing substitution by plastics, adhesives, and welding in some industries. Welding, particularly laser welding, is increasingly favored in automotive and aerospace sectors due to its ability to provide durable and reliable joints, representing competitive pressure to traditional mechanical fastening.

Adhesives and tapes are also gaining popularity, especially for noise, vibration, and harshness (NVH) reduction in vehicles. This trend is accompanied by increased demand for plastic fasteners as lighter, cost-effective alternatives to metal, especially where strength demands are moderate.

Innovation and Future Outlook

Manufacturers are investing heavily in research to develop innovative fastener designs, high-performance materials, and hybrid solutions to meet evolving industry standards and stringent quality demands. The integration of injection molding technology allows plastic fasteners to be produced in complex shapes tailored for specific applications, enhancing their adoption potential.

Additionally, sustainability concerns are prompting the fastener industry to explore eco-friendly materials and processes, further broadening the market scope.

In conclusion, the global fasteners market is set for healthy growth driven by expanding automotive production, infrastructure development, and technological advances in specialty and lightweight fastening solutions. While metal fasteners continue to dominate, extending application in construction and heavy machinery, the shift toward plastic and adhesive alternatives heralds a dynamic and evolving competitive landscape. The Asia-Pacific region, led by China and India, remains the market’s powerhouse, with Europe and North America following as large, mature markets pushing innovation and quality standards. This complex interplay of demand, materials, and application development promises a vibrant future for the fasteners industry.